Opinion: Refocus Required For Football Clubs

As BT Sport breaks another record for television revenue, this time for the UEFA Champions League and Europa League, the television purse continues to grow. But how long can it last, and what can clubs do now to ensure they’re not caught out when it does eventually subside? Atomic Sport director Ian Field investigates…

The warning signs are apparent. Football’s TV ratings are down across the board. Sky Sports has seen a 19% decline in Premier League football viewers from last year. It’s not a blip, it’s a long term trend; ratings for Sky’s flagship Sunday afternoon game shows a five-year decline with the average audience down 39% from 2011-12. On BT Sport, Champions League ratings are also down, obviously not helped by Manchester United’s non-participation. At least Europa League ratings are up.

Viewership stats are the usual pre-cursor to subscriber churn. The Chief Executives of Sky and BT have both been quoted in their intention to walk away should the price become too high. Shrewd pre-negotiating, perhaps, but it’s wise to be mindful that the edge of the cliff may be closer than we think. Globally and nationally, football continues to be consumed across an increasingly fragmented landscape of devices via a myriad of streaming and bite-size digital media, however digital monetisation models are not yet in place to compete with the traditional collective broadcast rights deals.

Faced with a potential drop in TV revenue, clubs will be wise to maintain focus on securing and maximising their other revenue streams; commercial and matchday revenue. In the past five years broadcast revenue has grown by 71% in the Premier League. Commercial revenue growth has also been strong. Premier League clubs have collectively grown their commercial revenue by 54 percent. This growth was stronger at the top end of the Premier League, the clubs with the most powerful brands and wider global appeal able to segment their commercial offerings across geographies and sectors in order to maximise commercial gains.

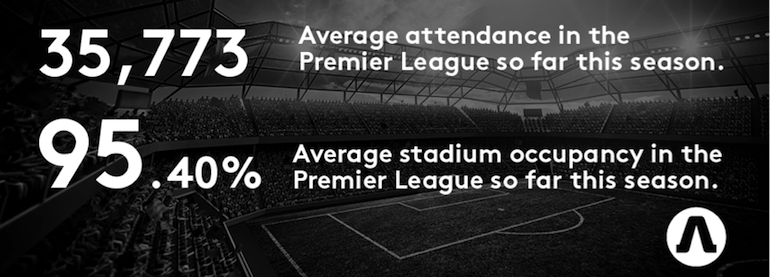

Matchday-income in 2015-16 accounted for approximately 14% of revenue for Premier League clubs. This has fallen from 23% in 2012-13 with the growth in broadcast revenue. In absolute terms matchday income has grown 4.3% from £585m to £610m over the same period. We can take a view on likely matchday revenue outcomes this season with approximately two-thirds of this season run. The hectic Christmas and New Year period is well behind us and the ‘business end’ of the season is in sight.

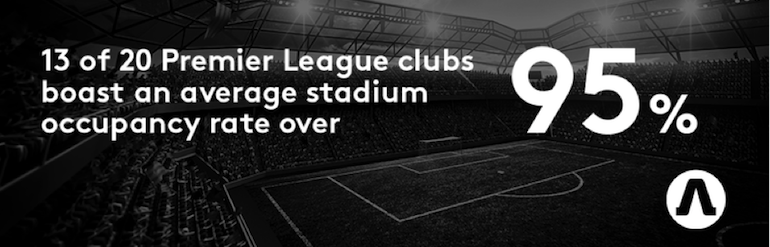

The overarching attendance trends in the Premier League and Championship remain constant. The Premier League continues to track at approximately 95% stadium utilisation. Thirteen of the twenty Premier League clubs boast stadium occupancy rates of over 95%.

There are six Premier League teams with an average stadium occupancy of over 99%. Of these West Ham Utd currently lead the way with 99.94%. Utlilising proactive promotion and discounting, West Ham has done a superb job of regularly filling the London Stadium to capacity despite the teething problems experiences in migrating and integrating the Upton Park fan base.

Hull City have the lowest average occupancy with the difficult relationship between the club’s owners and the fans having an obvious effect. Sunderland and West Brom also have stadium utilisation figures between 80 and 90%. Sunderland can certainly be commended for achieving the sixth highest average attendance in the Premier League at the 48,707 capacity Stadium of Light. West Brom’s performance is more surprising having enjoyed a good season on the pitch so far, they lay on the fringes of the race for a Europa League place. Yet they are currently tracking almost 5% down on last season’s 92.02%. Perhaps Tony Pulis’ effective but pragmatic style of play has come at a cost.

In the Championship, the season average to date is 71.10% stadium utilisation, which is up 6% on last year’s season average of 65.46%. This figure is bolstered by the presence of well-supported clubs such as Newcastle Utd, Aston Villa and Norwich City.

Aston Villa boast the second biggest stadium in the division and the second highest average attendance. But it’s been a disappointing season so far on the pitch with a rebuilding job underway with Steve Bruce. There’s plenty of scope to build off the pitch too as their stadium occupancy this season currently stands at 75.47%.

The overall Championship occupancy figures are certainly boosted by the performance of both Newcastle Utd and Norwich City, both of whom continue to fill their stadiums. Whilst high-performing Newcastle and Brighton & Hove Albion battle it out for the Championship title, it’s perhaps a little surprising that Norwich City are not closer to the promotion picture.

Attendance tracking in the Championship also reveals the importance of the bumper programme over the festive season. A review of the impact of the festive games from an attendance perspective reveals an almost universal Christmas bounce for those teams at home over the festive period.

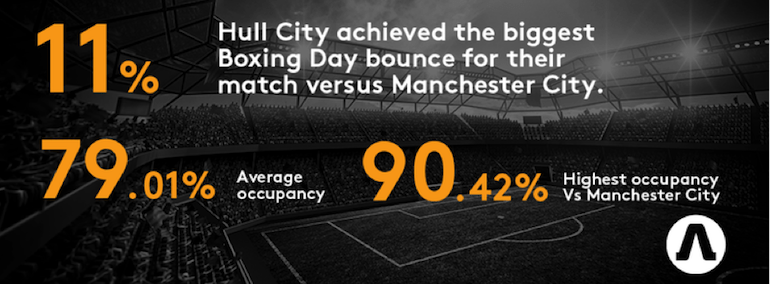

In the upper echelons of the Premier League, stadium utilisation is maintained in the high nineties across the season. Of the clubs in the Premier League with an average occupancy of under 95%, all four clubs that hosted home games experienced a Christmas bounce in attendance. Burnley had a full house against Middlesbrough on Boxing Day. Sunderland saw 95.46% occupancy against Liverpool, Southampton were at 97.44% against Spurs on the 28th December whilst Hull City achieved 90.42% against Man City, up 11% on their average stadium utilisation.

The Christmas bounce was even more pronounced in the Championship. The machinations of the Championship schedule dictated that six clubs did not host a fixture over the Christmas break. Of those 18 clubs that hosted at least one festive fixture, 16 achieved attendances over and above their average.

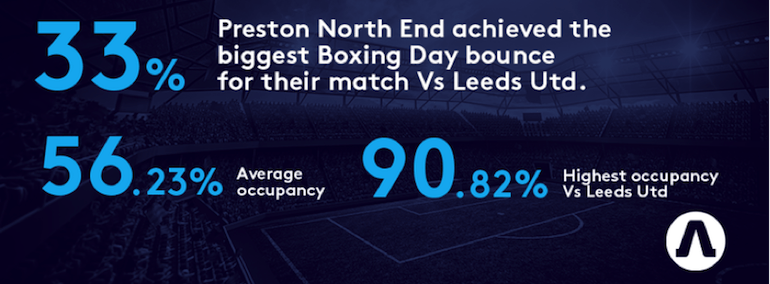

The biggest bounce occurred at Deepdale as Preston hosted Leeds Utd on Boxing Day and achieved an uplift of 33% from an average occupancy of 56.23% to 90.82%. The following game against Sheffield Wednesday saw a more modest 7% uplift. Aston Villa enjoyed a 23% uplift for the Boxing Day visit of Burton Albion whilst Blackburn Rovers saw a 22% increase for the visit of Newcastle on Boxing Day.

Appetite for Christmas football highlights the potential for clubs to achieve incremental ticket sales and bolster their matchday income. A question for the longer term is whether clubs are doing enough with their marketing programmes to convert floating fans to more regular visitors?

Several key trends are apparent from the data. Stadium occupancy from the top of Premier League to lower mid-table is very consistent; 13 of 20 Premier League clubs boast an average stadium occupancy rate over 95%. However for the bottom end of the Premier League and the Championship in particular, the situation is far more variable with 63% of the Championship (14 teams) under 80% occupancy. It’s clear that football clubs outside of the Champions League elite can do much more with their brands to drive both commercial and matchday revenue. Whilst club-marketing and commercial departments are often stretched in terms of resources and targets, significant incremental revenue opportunities can be achieved with optimisation of brand activity including season ticket and matchday pricing strategies.