Making sense of sport’s value proposition (2/4)

According to The Sport Industry Report 2025, the biggest challenge to investment comes from long-term disruption in sport’s most important partner industry.

Media rights income, currently worth an estimated 39% of the average sports team owner’s revenue per annum, has grown quickly and reliably over recent decades.

To cite examples from the UK’s three leading team sports: from 2013 to 2023, the Premier League achieved a compound annual growth rate (CAGR) of 11% for its media rights income; the CAGR for the England and Wales Cricket Board’s (ECB) fees was 9.6%; Premiership Rugby’s was 8.7%.

Today, however, that progress has slowed. Media companies have become much more conservative in their spending on sport, facing a combination of pressure from lower-cost streaming platforms, cooling customer demand, and rights prices that had been driven to unsustainable heights by earlier competition.

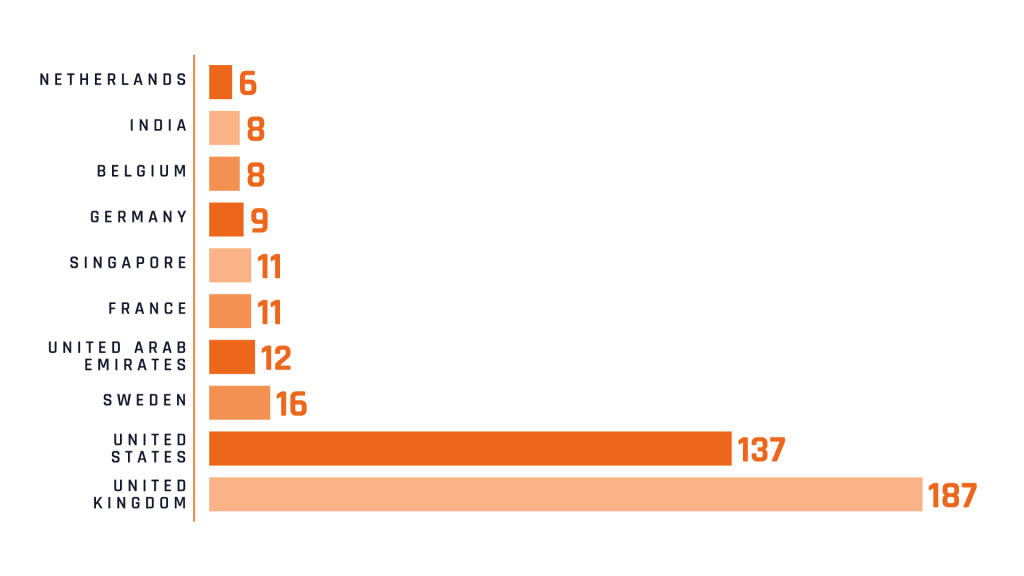

When it comes to deal origination, it pays to be close to the ground. Despite the long tail of global investors in the UK, 56% of all deals were backed by European investors – the bulk of which identify as VC funds or strategic acquirers. However, non-European investors cumulatively contributed 21 deals to the 291 originated from EMEIA-based investors.

This includes investors ranging from sovereign wealth funds typically seeking exposure to sports IP owners, to a string of UAE-headquartered VC funds with investment focuses ranging from childhood development to blockchain-enabled fan engagement. Source: EY, Pitchbook

Only 2% of UK sports rights holders believe media rights have major growth value potential over the next five years – a considerable risk factor with many high-profile rights deals up for renewal in the mid-2020s.

As they approach this ‘contract rights wall’, rights holders must navigate a very different commercial landscape – a new world where many media companies will be pursuing one of two acquisition strategies.

The first of these can be called a ‘Moneyball strategy’, where media companies prioritise rights for cheaper, underpriced or overlooked sports properties. The intention of this is to cultivate a customer base that, in the aggregate, can replicate the lifetime value of viewers and subscribers attracted to their channels in the previous era.

The second approach is a ‘polarisation strategy’, whereby media companies clear resources to attack the most expensive rights and balance out their offering with deals for much smaller sports with an established audience and demonstrable ROI. The upshot of this will be that those rights holders in the middle, whose properties might have been seen as adding value to consumers in the pre-streaming bundle era, could be squeezed out.

Rights holders must demonstrate an excellent understanding of their audience, and the wherewithal to bring in new and engaged fans, to compete in what has become a buyer’s market.

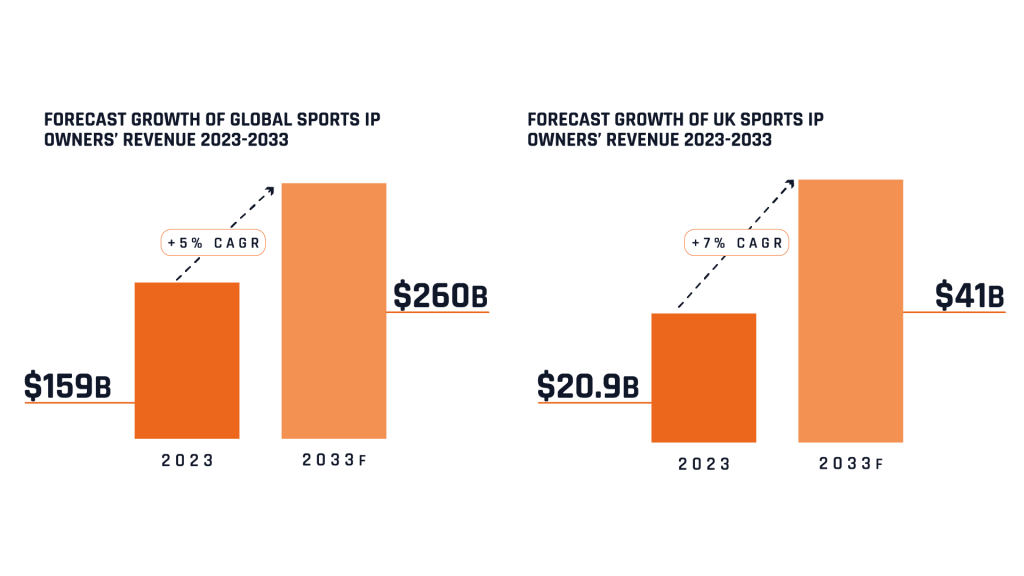

Despite this, domestic sports IP owners are forecast to increase annual revenues by $20 billion between 2023 and 2033.

Without the guarantee of appreciating media contracts, maximising fan engagement and optimising more powerful commercial partnerships will be critical if sports owners are to sustain topline growth over the next decade.

The biggest beneficiaries will be the fans, as the most successful IP owners will be those that prioritise fans and place them at the core of their strategies.

But investors will want to see revenues diversified as unrealised value is captured from other activities: building bigger engaged audiences, creating new non-matchday experiences and products, improving direct-to-fan income opportunities, and growing sponsorship returns through an enhanced offering to brands.

Without the guarantee of appreciating media contracts, maximising fan engagement and optimising more powerful commercial partnerships will be critical if sports owners are to sustain topline growth over the next decade. The biggest beneficiaries will be the fans, as the most successful IP owners will be those that prioritise fans and place them at the core of their strategies.

This is an extract. To read in full, download the Sport Industry Report 2025.