Amidst a return of investors to the deal table, the UK sports industry will remain a critical focus for institutional investors in 2025 – not least for those investors willing to embrace new business models and diversify income streams.

Analysis by EY for The Sport Industry Report 2025 confirmed a surge of institutional investment over the last five years. Since 2019, $160 billion has been committed across 7896 deals in Europe, with more than 35% involving UK-based assets.

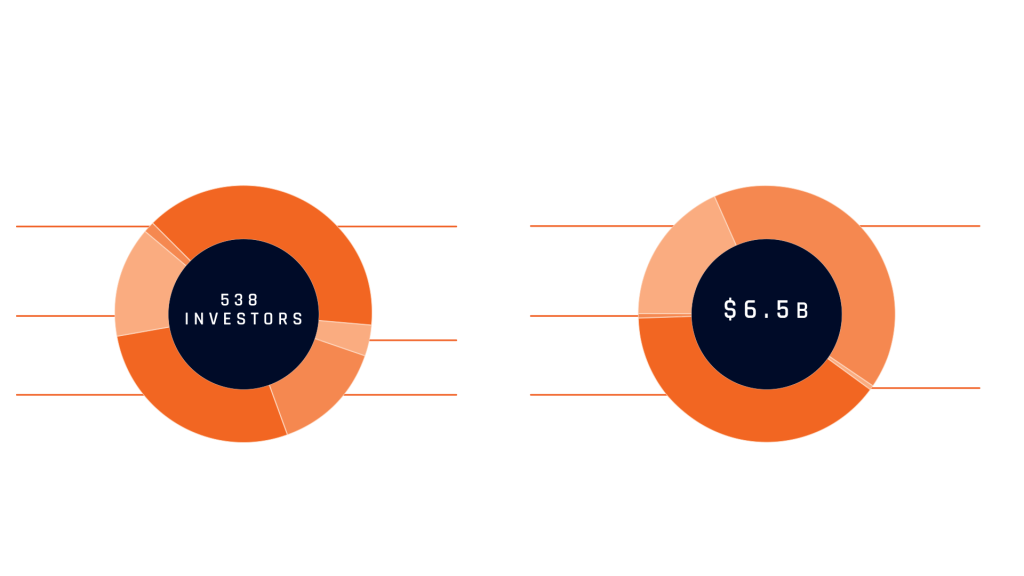

Globally, investors now view sports teams and businesses not just as trophy assets but as a source of outsized potential returns, a means of diversifying portfolios, and a hedge against macroeconomic risk thanks to inelastic demand. As a result, investment is flowing into UK sport from a healthy mix of sources with $6.5 billion committed across 375 deals in 2023/24, a significant underestimation given the number of deals with an undisclosed value.

Strategic investors, private equity and venture capital have come to the fore as the influence of family offices and high net worth individual’s wanes. Sovereign wealth funds – typically involved in fewer, larger deals – are also more active in the UK than elsewhere in Europe.

The following investment analysis defines the ecosystem across three broad categories:

1. Sports entities that hold sporting rights or IP, such as clubs, leagues, federations and events.

2. B2C commercial partners that leverage sports content and communities such as broadcast media, gaming and immersivity, retail, hospitality and travel, health and nutrition.

3. B2B service partners that partner with sports client, such as media and technology solutions, fan engagement services, agencies, data and analytics, ticketing, venue management and other logistics.

The surge in sports dealmaking activity in the last five years reflects a broader trend where sports entities are increasingly viewed as a lucrative investment opportunity, driven by rising valuations and potential for substantial returns.

While momentum has flattened amid a wider downturn in overall M&A activity, the UK continues to contribute a considerable share of deal flow in Europe. At the forefront of this drive is the most popular sport in the UK: football. One notable dynamic responsible for this uptick is the growing prevalence of multi-club ownership (MCO) structures across the sport, which strategic and PE investors are increasingly leveraging to unlock cross team synergies. Source: EY, Pitchbook

Despite contributing a relatively small source of capital via direct and co-investments, sovereign investors remain a key source of capital to leading assets. Having already acquired stakes in leading assets across multiple sports leagues, teams, and the wider media ecosystem, sovereign investors continue to actively source opportunities for deployment in neighbourhoods ripe for investment. Source: EY, Pitchbook

This is an extract. To read in full, download the Sport Industry Report 2025.