Part 3: Making sense of sport’s value proposition

According to The Sport Industry Report 2025, The global leader in sports investment on both the buy and sell side is the US, where larger local markets and the certainty of closed leagues bolster asset values.

Changing UK dynamics

Nonetheless, the UK recorded $2.8 billion in team and league investments in 2023/2024. – a likely underestimation, given that many larger deal values are undisclosed.

This is a market with some distinctive qualities. Football’s professional pyramid, for example, promises huge growth potential for shrewd investors who can bear the downside risk of relegation.

The recent strides made under American ownership by clubs like Wrexham AFC and Ipswich Town give an indication of what international backers might hope to accomplish. Each operates under very different financial models, but both have managed successive promotions.

They have also shown that entertainment-based brand-building exercises are possible from the lower tiers: through A-list owners and a Disney documentary series in Wrexham’s case, and a formal partnership for Ipswich with singer and supporter Ed Sheeran.

According to UEFA, England also has the most teams involved in multi-club organisation (MCO) structures – seen as a route to establishing commercial synergies, brand scalability, and pooled talent development capabilities.

MCOs can also expand the range of opportunities for multiple participants to invest. The multinational City Football Group – which grew out of the sovereign backed Abu Dhabi United Group’s ownership of Manchester City – now counts US buyout shop Silver Lake, and Chinese-based strategic investors China Media Capital and CITIC Capital among its stakeholders.

The activities of football’s incoming independent regulator will therefore be watched with some interest, as that body explores firmer regulations and competitive protections. More broadly, the still-climbing cost of player transfers and salaries could further raise the barrier to entry for team owners.

Outside of football, rights holders are developing properties that hew closer to the US model, by introducing closed competitions where the financial risk associated with relegation and promotion systems is removed entirely. Cricket’s franchise-based competition, The Hundred, is an early example – the ECB is currently marketing 49% stakes in each of its eight teams to interested parties in an auction being overseen by the Raine Group.

Media reports have suggested interest from a range of high-profile parties, spanning major PE shops based in the US, to strategic investors such as those existing owners of teams in the Indian Premier League, which might further accelerate the consolidation of cricket’s T20 franchise marketplace.

It remains to be seen whether the ECB can exploit these varied dynamics to realise its £350 million target from those sales, but it seems likely that more rights holders will explore creating US style walled gardens around their competitions. Other models will also emerge as sports bodies try to establish and control monetisable IP: 50% of the Professional Triathletes Organisation, headquartered in London, is owned by its athletes, with the other 50% sold to investors.

The pace of development in the women’s sports sector will also be highly pertinent. Its global value is projected to grow from $1 billion in 2023 to a remarkable $23 billion by 2033.

That could indicate real upside not only for organisations with existing women’s teams – including the Hundred and professional football clubs – but also for startup properties.

Investment in wider ecosystem

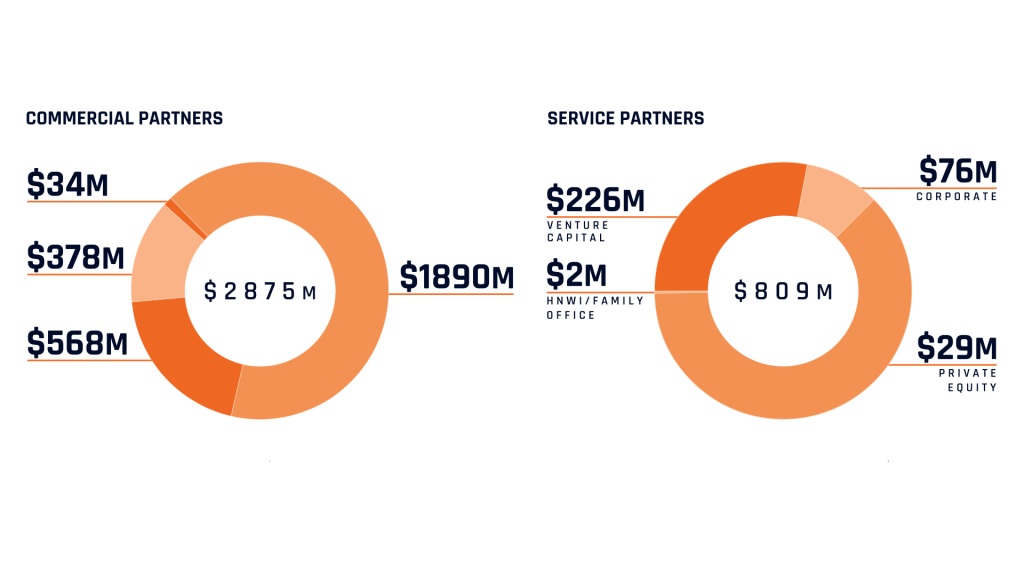

Amid these shifting income priorities, the health of the UK sports economy is ever more dependent on other businesses. Service partners received over $800 million of investment in the last financial year, with commercial partners driving $2.875 billion worth of deals. Some of that growth can be attributed to synergistic opportunities across sport and adjacent lifestyle verticals. One in three commercial partnership transactions were part of ‘buy-and-build’ strategies of bundling complementary assets, while there is continued consolidation among the agency landscape where client ambitions to expand into other verticals requires more specialist skillsets from the organisations that serve them.

Commercial partners with the capabilities to scale fan reach, optimise content distribution, and create new verticals for cross-selling provide ample opportunities for incumbents to scale into adjacent markets. The combination of digital transformation, heightened consumer interest, and strategic collaborations with sports entities positions have poised commercial partners for continued growth. Areas like sports media, gaming, Web3, sports retail and consumer health and nutrition are expected to continue to be attractive investment avenues.

Prospective service partners continue to attract interest from investors, particularly those with the necessary digital expertise to optimise analytics and drive fan engagement. Global investors are capitalising on the surge in streaming service technology and on-demand content platforms by targeting commercial rights licensing and broadcasting opportunities. This, along with the boom in betting, fan engagement, media and performance, has made this segment attractive for investors.

This is an extract. To read in full, download the Sport Industry Report 2025.